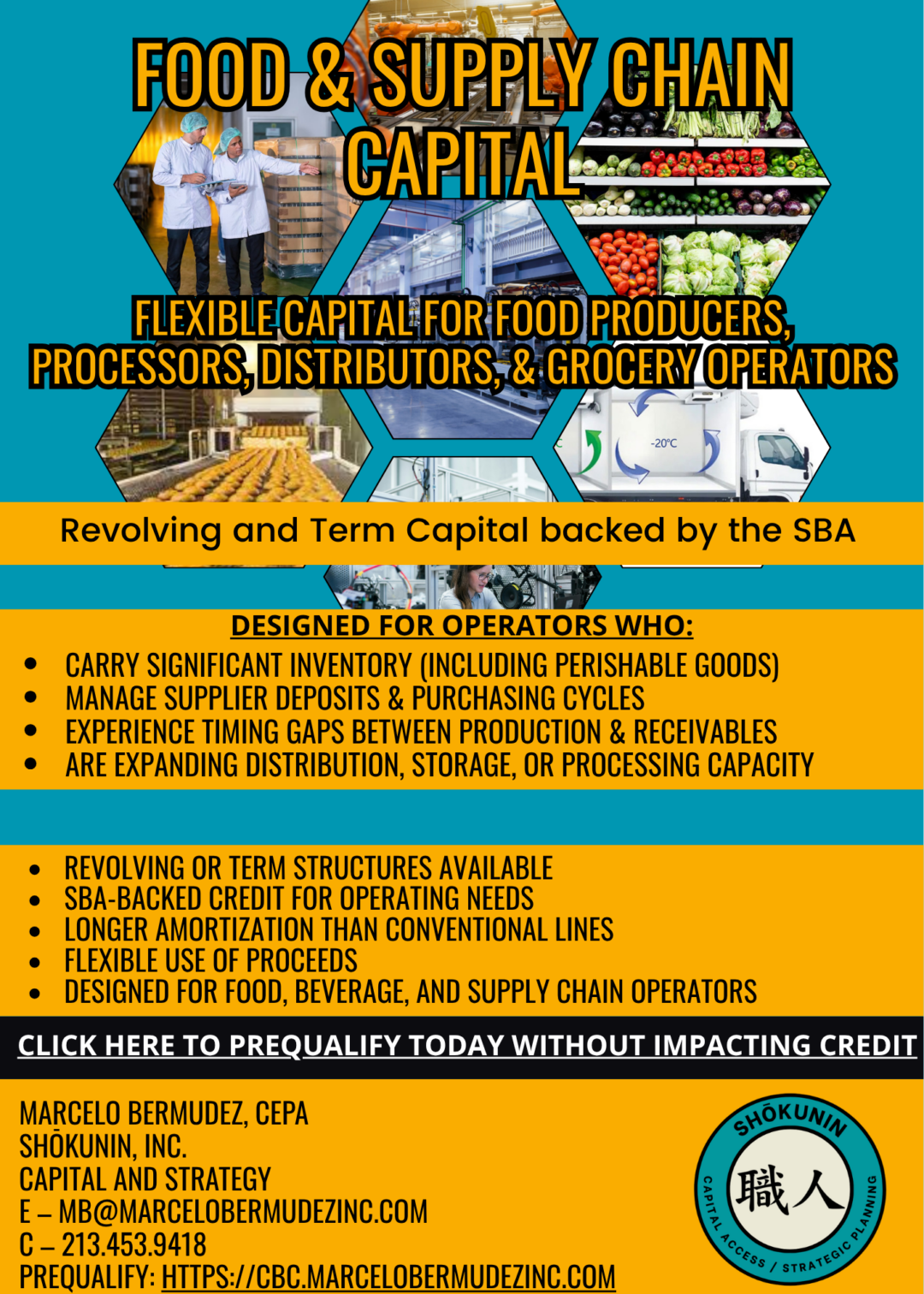

A policy change that matters more than the headline suggests.

The SBA recently expanded its guarantee coverage for lending to grocery retailers, food producers, processors, and supply chain operators, moving from 75% to 90% on qualifying loans. The announcement framed it as a response to food prices. That is accurate, but it is not the whole picture.

What changes is the math inside a lender’s credit decision.

When loss exposure drops by that margin, deals that previously failed credit committee review become approvable. The business did not change, but the risk calculus did. That is a meaningful shift for operators who have been told no, or told to come back with more collateral, more history, or a cleaner balance sheet.

Who This Applies To

Food and supply chain businesses occupy a difficult position in conventional lending. They carry significant inventory, often perishable. They manage timing gaps between what they spend and what they collect. They are operationally intensive and asset-heavy, and their financials can look uneven during growth phases even when the underlying business is sound.

Those characteristics have historically made lenders cautious.

The 90% guarantee does not change those characteristics. It changes how lenders are willing to weigh them. For businesses in this space, that translates into a few concrete things: more tolerance on leverage, more flexibility on forward projections, and more willingness to lend through a growth phase rather than waiting for full stabilization.

Structures Available

The SBA-backed programs applicable here include both revolving lines and term structures. Revolving credit works for businesses managing inventory cycles and supplier timing gaps. Term structures work for capacity expansion, cold storage, processing equipment, distribution buildouts.

Loan terms are longer than conventional lines, which matters for cash flow (10 years versus 3 or 5 years). Proceeds can be applied across operating needs, equipment, or working capital, depending on how the deal is structured.

How to Position Your Business

The guarantee is stronger. Access is still earned.

Lenders will still want a clear financial narrative: how revenue is generated, what the cost structure looks like, and how debt service fits into operations. Businesses that can present that picture cleanly will move faster and get better terms.

If your financials are in order but you have been declined before or told the deal needs more seasoning, this is worth revisiting. The criteria have shifted enough so that conversations that stalled may open differently now.

What We Do

We work with food producers, processors, distributors, and grocery operators on SBA-backed financing, from initial eligibility review through deal structuring and lender placement. If you want to understand whether this program fits your situation, the prequalification process does not affect your credit and takes under ten minutes.

Marcelo Bermudez

Shōkunin, Inc. – Capital and Strategy

213.453.9418