I didn’t attend the Restaurant Finance and Development Conference in Las Vegas this year, but a friend shared his notes. What stood out was how closely those sessions mirrored what I am seeing every day with operators, lenders, and franchise platforms trying to scale.

The restaurant industry has always been a story of courage. Today, creativity is no longer optional. Margins are thin, capital is cautious, and the room for error has narrowed to inches.

Yet the groups that understand the landscape are still growing. The gap is no longer one of size, but rather of strategy, capital discipline, and the ability to adapt quickly.

Pain Point 1: Expansion Dreams vs. the Cost to Build

Operators want to grow. The growth-mindset hasn’t changed. The math has.

From the developer’s perspective, land is expensive. Construction is even worse. New builds rarely pencil unless the operator has an extraordinary rent deal or a low land basis. That is why second-generation spaces and inline retail locations are becoming the new development pipeline. They let operators to expand, lower capex, shorten the time to revenue, and reduce the risk profile of the transaction.

This shift is not cyclical. It is structural. The groups that learn to thrive in second-gen environments will pull ahead.

Pain Point 2: Capital Is Tight, Even When It Shouldn’t Be

I just got off a call with a lender who declined an 18-unit food & beverage franchise platform. The group was profitable. They had scale. Their home state was offering an 80 percent guarantee. They are even on the SBA-approved franchise list which means they’ve gone through the hurdles of showing they’re a viable brand.

The lender still said no. The borrower put in 20 percent of his own capital and was on track for a 2.2X DSCR within 15 months. It didn’t matter.

Five years ago, that deal would have received multiple offers. Today capital has become more selective, more compliance-driven, and less willing to underwrite younger platforms, even with substantial guarantees.

Pain Point 3: Working Capital Is Still the Silent Killer

The consumer is becoming more selective. Inflation continues to shape discretionary spend. Operators who run too thin on liquidity learn fast that the market has no patience for them.

This is why many are turning to the only “cheap” capital left: the sale-leaseback. It remains one of the most cost-effective ways to unlock trapped equity, particularly for operators with established real estate footprints. It remains a viable lever, but it must be used intentionally. Once you sell your dirt, you only get one shot at the proceeds.

Pain Point 4: Tariffs Are Back and Hitting Equipment Costs Hard

Tariffs have resurfaced, and since so much FF&E and equipment originates from China, operators are experiencing unexpected budget creep. New store costs were already high because modern fast-casual model relies heavily on experience, design, and throughput. With equipment and buildout costs up 20 to 35 percent over pre-2020 levels, even an operator projecting an 18% net margin feels immediate pressure. The operators who rely on precise budgets or who need two- or three-year pro formas to hit exact return thresholds are having to reset expectations.

Countering the “It’s Just F&B, It Can’t Work” Mindset

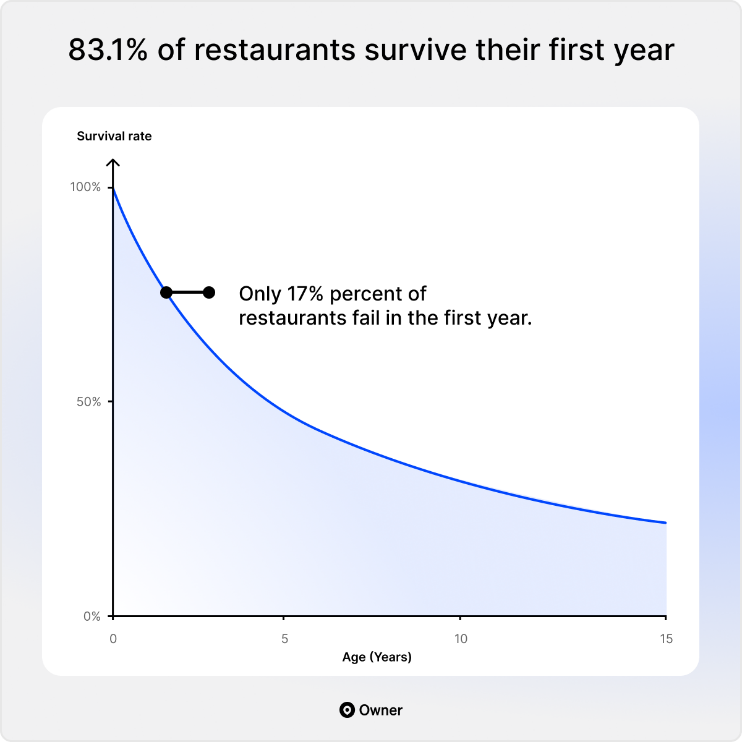

Here’s where things get interesting. I have heard too often from lenders and capital providers the off-hand line: “Well, it’s food and beverage. That business always fails.” It’s a lazy mindset. The data tells a different story.

-

Contrary to the oft-quoted myth that “90% of restaurants fail in the first year,” actual research indicates only about 17% of restaurants fail in their first year. Owner.com

-

Even more telling: about 51% of restaurants survive past their 5th year. Owner.com

-

Furthermore, in some markets using platform data, such as from DoorDash, survival rates for one year are above 90–95%. For example, Detroit had a 94.4% one-year survival rate. Axios

That means this business is not inherently doomed. It means the industry is complex and demands the right operator, real execution, and a smart capital stack. It’s not a category that should automatically be dismissed.

So when capital providers say “food & beverage is too risky,” what they’re really saying is “we don’t understand this business well enough” or “we don’t want to allocate the time and risk premium.”

That’s their choice. Smart operators will pick off the deals those lenders won’t touch.

Opportunity 1: Strong Operators Are Still Scaling

Even in this environment, we are helping a 20+ unit franchisee recapitalize through a $5 million offering. They are using the capital to eliminate high-cost legacy debt and create an additional $2.5 million working capital reserve to expand at three to four locations per year.

Why does this deal work while others stall? A few reasons:

-

They run with clean financials

-

They have tight unit economics

-

They understand development pacing

-

They resource their growth with the right capital stack

-

They communicate clearly with lenders and investors

Discipline creates opportunity.

Opportunity 2: Second-Gen Real Estate Is the New Growth Engine

Inline and second-generation stores offer:

-

Lower build-out costs

-

Faster openings

-

Less financing friction

-

More flexibility in market selection

Operators who stop chasing ground-up monuments and instead focus on adaptable footprints will gain a strategic edge.

Opportunity 3: Capital Partners Still Want Good Stories

Investors are not pulling back. They are repricing risk. The platforms that can tell a coherent capital story will continue to attract capital. That story needs to include:

-

Transparent financials

-

A clear development plan

-

Realistic unit-level economics

-

A capital stack that matches the timeline

-

A path to discipline before a path to scale

The deals that die today do not die because the operator is bad. They die because the story is incomplete.

The Real State of the Industry

The conference notes summed up the industry perfectly. Realistic but optimistic. Tough but resilient. Challenging but still full of opportunity.

This is not an industry in decline. It is an industry in transition.

The operators who embrace the shift, who tighten their execution, who build smarter rather than bigger, and who treat capital as a strategic partnership rather than a transaction will be the ones still standing five years from now.

Everyone else will look back and realize the headwinds weren’t the problem.

The lack of strategy was.